How Long Does It Take to Build 20% Equity in Your Home?

How Long Does It Take to Build 20% Equity in Your Home?

For many homeowners, 20% equity is a powerful milestone.

It’s the point where many lenders will allow you to remove private mortgage insurance (PMI), it increases your financial flexibility, and it gives you access to tools like home equity loans or HELOCs.

But one of the most common questions buyers ask is:

How long does it actually take to build 20% equity in a home?

The answer depends on three major factors: your down payment, market appreciation, and improvements you make to the property.

In many cases, homeowners reach 20% equity much faster than they expect.

What Does 20% Equity Mean?

Equity is simply the difference between your home’s market value and what you still owe on the mortgage.

For example:

Home purchase price: $300,000

Mortgage balance: $240,000

Your equity would be:

$300,000 – $240,000 = $60,000

In this example, the homeowner has 20% equity in the property.

This is why lenders often view 20% as an important threshold. It reduces lender risk and unlocks financial advantages for the homeowner.

The Traditional Timeline to Reach 20% Equity

Historically, homeowners who purchase with a smaller down payment (3–5%) may expect it to take 7–10 years to reach 20% equity through mortgage payments alone.

Why does it take that long?

Because in the early years of a mortgage, most of your payment goes toward interest instead of principal.

This means the loan balance decreases slowly at first.

But this is only part of the story.

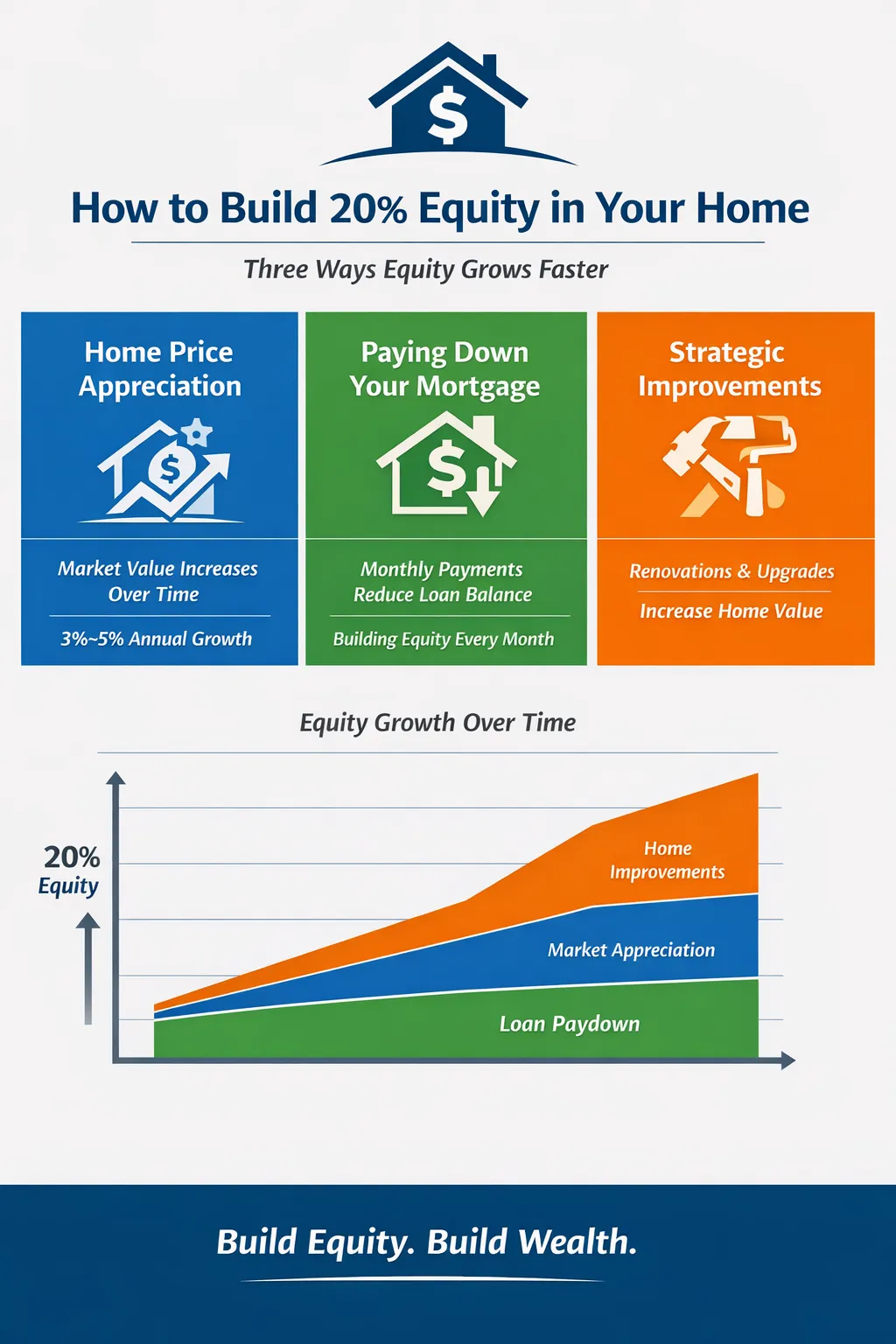

The Three Ways Homeowners Build Equity Faster

Most homeowners reach 20% equity faster because equity doesn’t only come from paying down the loan.

There are three powerful forces working in your favor.

1. Home Price Appreciation

Over time, real estate values tend to increase.

Historically, U.S. home values have appreciated about 3–5% per year on average, although some markets grow faster during strong housing cycles.

For example:

Purchase price: $300,000

If the home appreciates 4% per year, the property value after five years could be approximately:

$365,000

Even if the mortgage balance only drops slightly, the increase in value dramatically boosts equity.

2. Paying Down Your Mortgage

Each monthly mortgage payment includes a portion that reduces the principal balance.

As the balance decreases, your ownership share of the property increases.

Over time, more of each payment goes toward principal rather than interest, which accelerates equity growth.

3. Strategic Home Improvements

Many homeowners accelerate equity growth through targeted renovations.

Some improvements can significantly increase a home's market value, including:

Bathroom upgrades

Kitchen renovations

Interior painting

New flooring

Improved curb appeal

These improvements can create what real estate investors call forced appreciation, where property value increases faster than the market alone.

A Real Example of Equity Growth

Recently, I worked with clients who purchased a home for $260,000.

The property needed cosmetic improvements, so they invested about $33,000 updating two bathrooms and repainting the interior.

They lived in the home for four years.

When they sold the property, the home sold for $400,000.

While market appreciation played a role, their improvements and strategic purchase also contributed to the equity growth.

This example highlights an important lesson:

Sometimes the best investment you make is the home you live in.

Can You Reach 20% Equity in Just a Few Years?

Yes—many homeowners reach 20% equity within three to five years, especially if one or more of the following occurs:

The local housing market experiences strong appreciation

The homeowner makes strategic improvements

The buyer purchased the property below market value

The buyer made a larger down payment

Real estate markets can accelerate equity growth far beyond what mortgage amortization alone would produce.

Why Reaching 20% Equity Matters

Once you reach 20% equity, several financial benefits may become available.

Removing Private Mortgage Insurance (PMI)

Many conventional loans allow homeowners to remove PMI once they reach 20% equity, which can reduce monthly mortgage payments.

Access to Home Equity

Homeowners may qualify for:

Home Equity Loans

Home Equity Lines of Credit (HELOCs)

Cash-out refinancing

These tools allow homeowners to leverage their property value for investments, renovations, or other financial goals.

Greater Financial Security

Equity provides a financial cushion and increases your overall net worth.

The Investor Mindset

One of the biggest differences between typical homebuyers and experienced real estate investors is how they evaluate a property before purchasing it.

Most people shop for homes.

Investors analyze them.

They ask questions like:

What improvements will increase value?

How strong is the local housing market?

What will this home be worth in five years?

When you approach homeownership with this mindset, your home becomes more than a place to live.

It becomes a wealth-building asset.

The Bottom Line

Building 20% equity in your home can take seven to ten years through mortgage payments alone.

But when you factor in market appreciation and strategic improvements, many homeowners reach that milestone much sooner.

In fact, in strong housing markets, homeowners may build 20% equity within just a few years.

Your home can either be a place you live, or it can be a powerful financial asset that builds wealth over time.

Often, the difference comes down to how the property is evaluated before you buy it.

Frequently Asked Questions

How long does it usually take to reach 20% equity?

For many homeowners, it can take 7–10 years through loan payments alone, but appreciation and improvements can shorten the timeline significantly.

Can renovations increase home equity?

Yes. Strategic renovations like kitchen upgrades, bathroom remodels, and interior improvements can increase a home's market value and accelerate equity growth.

What happens when you reach 20% equity?

Many homeowners can remove PMI, access home equity financing, and increase their overall financial stability.